Never Miss a Tax Notice Again

Automate tax notice intake at scale, streamline resolution workflows, and keep a clean audit trail.

Automate tax notice intake at scale, streamline resolution workflows, and keep a clean audit trail.

Active users

Notices processed

AI accuracy

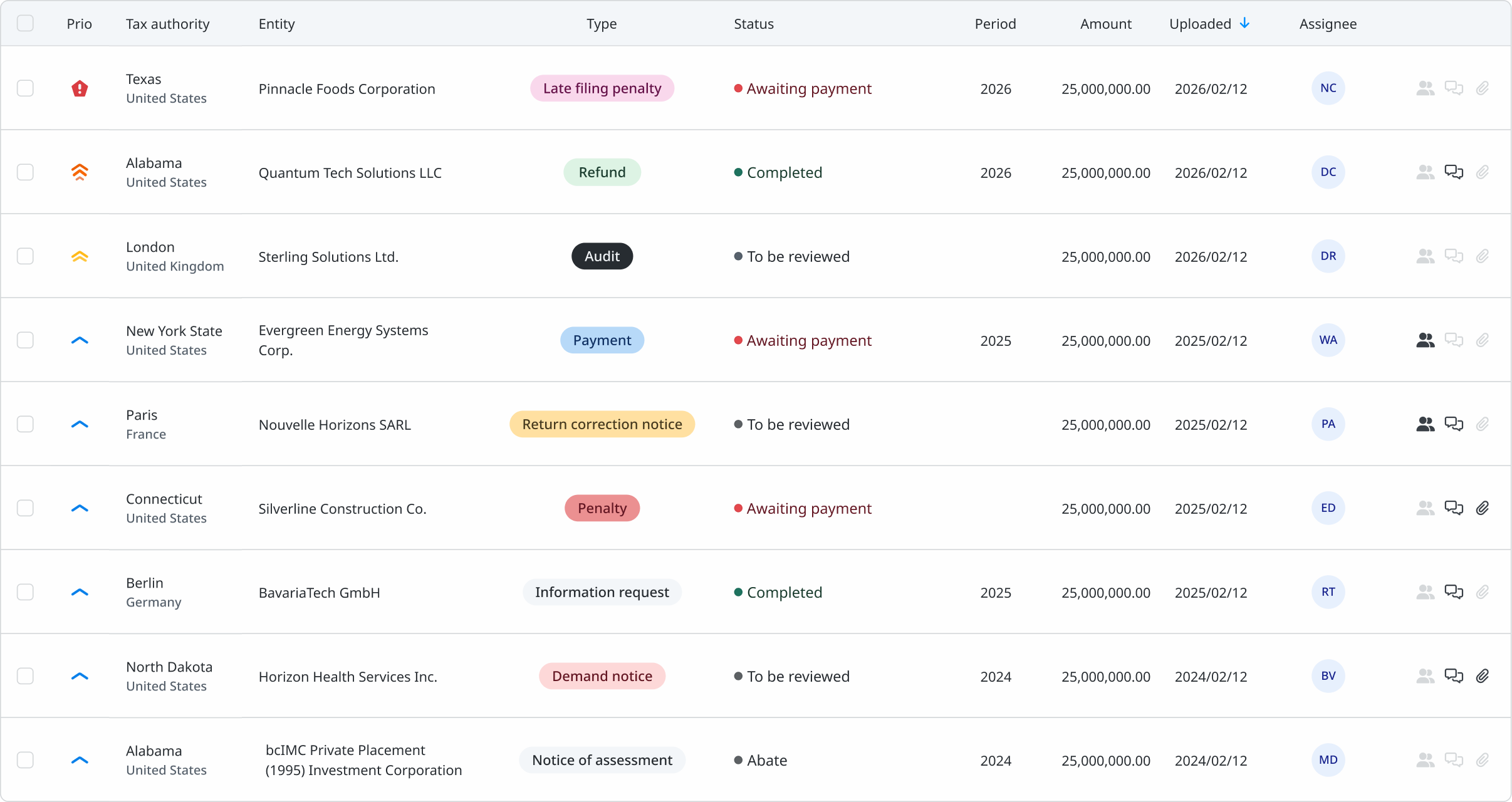

Eliminate manual handling with automated notice intake and organization. Work with your team and external advisors, assign tasks, leave notes, and keep everything in one place.

Noticehub monitors due dates, escalates priorities as they approach, and sends automated reminders to keep your team on track, even during the busiest periods.

Keep everything in one place. Notices, documents, task assignments, statuses, and actions are stored in a single secure repository, so your team always has a reliable record to work from.

Always know what happened and when. Every action taken on a notice is logged with a full time-stamped history, giving you a reliable audit trail for internal controls, audits, and smooth handovers.

Noticehub has transformed the way we handle tax notices by providing a centralized platform for our team. It streamlines the upload, categorization, and review process, allowing us to act faster and with greater accuracy across jurisdictions.

Amelia Staton

Indirect Tax Analyst

TDW (US) Inc.

Noticehub provides us with a central place for the tax team to upload and manage the many notices that we receive from tax authorities globally. It is able to quickly read and interpret each notice and organizes them for easy review and action across the team.

Derek Chan

Former Managing Director, Tax

Northleaf Capital Partners

Drag and drop your scanned tax notice PDFs onto the dashboard, whether single, in batches or even multiple notices in one PDF file.

Automatically separate, translate, and extract key data from every notice in seconds.

Capture all critical tax data instantly, from entities and deadlines to amounts and notice types.

Pre-filled data lets you review faster and confirm accuracy with full confidence.

Automate and customize workflows, collaborate on notices and maintain full visibility across every step.

Stay ahead with real-time notifications, deadlines, and actionable reporting.